- Ethereum’s greatest strength is its ability to adapt without losing coherence, evolving through cultural forks, architectural pivots, and economic redesigns that most platforms wouldn’t survive.

- Ethereum’s architecture and economic model has pivoted a few major times to combine network adoption and value capture, and improve validator and user experience.

- With regulatory clarity, stablecoin rails, DeFi dominance, RWA applications and ETF flows converging, Ethereum isn’t chasing the next narrative—it’s aiming to become the institutional foundation that underwrites it.

1. Genesis: Programmable Money Emerges (2015)

In October 2013, Vitalik Buterin visited the Mastercoin team in Israel. When his proposed upgrades were rejected, he branched off to design Ethereum (coincidentally, just a few blocks from where Bitwise was later founded in 2017, in San Francisco).

Co-founders Gavin Wood and Charles Hoskinson (now of Polkadot and Cardano) joined Buterin, along with Jeff Wilcke, to define Ethereum's base-layer primitives: a virtual machine to execute smart contracts, gas limits to meter compute, and a consensus protocol to validate blocks.

Ethereum launched on July 30, 2015, with around 30 contributors and a roadmap including four core upgrades: Frontier (basic mining), Homestead (network reliability), Metropolis (user interfaces), and Serenity (Proof of Stake, later named The Merge).

During each phase, Ethereum laid the foundations of its mission to becoming a decentralized, global financial operating system.

2. The DAO Hack: Resilience Through Forks (2016)

Ethereum's founding idea was clear: a decentralized, rules-based, global financial platform where software enforced trust, not institutions. The first large-scale application was “The DAO”, an experimental, community-run investment fund that raised $150m in ETH and aimed to invest in projects in the Ethereum space. A future was promised where capital allocation was governed by code, not corporations.

This trust was broken nine months post-launch. A vulnerability in The DAOs smart contract allowed an attacker to siphon $70M, worth 3.6M ETH.

Ethereum faced its first existential dilemma: should the community stick to the principle of “code is law”, or does it intervene to protect users and their assets.

A soft fork was proposed-a gentle upgrade that would freeze the stolen funds by blacklisting the hacker's address. In a soft fork, the network stays on the same chain, but different rules are introduced that older computers can still follow. Think of it like changing the rules of a football game without kicking anyone off the field.

But the attacker responded with a public bribe: promising to reward miners with the stolen funds who ignored the fork. That threat was enough to divide the community. Many miners and users chose to abandon the original chain and follow a new one that reversed the hack, much to the hackers' enjoyment.

This kind of split is called a hard fork-when the network breaks into two chains that no longer follow the same rules or history, and the computers on either chain cannot understand each other. Think of it like the original football game splitting into two, with the second football game implementing different rules the players of the first game don't understand.

At this point in time, there was a divergence in philosophy in the ecosystem, which caused the split. As a result, Ethereum Classic (ETC) was born. This community took the view that immutability rules. That trust in the system means accepting outcomes, even painful ones. ETC stood for purity of principle, but lost developer momentum, adoption and capital in the years to come.

Ethereum, however, chose social consensus over “code is law”, prioritising restoring stolen funds, preserving investor confidence and affirming that Ethereum was a community with agency. This foreshadowed Ethereum's attitude almost 10years later.

At first, investors and the community were unsure. ETC began trading in wide ranges between $0.84-$1.62, reflecting initial market uncertainty about the viability of the original chain.

The market ultimately validated Ethereum's hard fork as seen via the widening price delta between ETH and ETC. Over time, ETH has commanded an increasingly dominant premium representing more than just price appreciation-it reflects the market's recognition that Ethereum's willingness to take decisive action, prioritize user protection, and maintain community cohesion was the right choice.

The DAO incident institutionalised governance by debate and consensus, foundational for handling intense upgrades and issues in the future.

3. ICO Boom: Ethereum Becomes the Launchpad (2017)

Ethereum's first encounter with scale came in 2017, and it came fast. The ERC-20 standard turned Ethereum into the world's easiest token launchpad-allowing startups to raise capital directly from the crowd through Initial Coin Offerings (ICOs). Nine out of the ten largest projects that year chose Ethereum, collectively raising $603M, primarily in ETH.

But the velocity outpaced value. Many projects launched with little more than a whitepaper and a roadmap. The result was at once exhilarating, chaotic, and troublesome: a hypercompressed feedback loop of experimentation, speculation, and-ultimately-regulatory scrutiny. The SEC cracked down, halting the ICO boom, but not before Ethereum had already proven something deeper.

This short-lived frenzy became a stress test for Ethereum's infrastructure and a proving ground for novel fundraising models. Smart contracts scaled. Infrastructure held. Users learned. Founders iterated. The market rapidly separated substance from hype, offering a glimpse of what crypto capital formation could become.

More than just a fundraising frenzy, the ICO boom was Ethereum's first crypto product-market fit moment. Even failed ICOs revealed user preferences, tooling gaps, and latent demand. The frenzy seeded the platforms, frameworks, and developer muscle that would later give rise to more durable categories-like DeFi, NFTs, and tokenized assets.

In hindsight, the ICO cycle was a pivotal calibration event. It showed Ethereum could host global capital formation at scale, and established it as the de facto sandbox for crypto innovation.

4. DeFi Summer: A Parallel Finance System (2020)

After a bruising bear market from 2018-2020, Ethereum didn't just recover-it matured. DeFi Summer marked the protocol's second discovery of product-market fit. But unlike ICOs, where the focus was speculation, DeFi was different; The focus was real utility. Protocols like Uniswap, Aave, Compound, and Curve redefined capital markets from the ground up, enabling users to swap, lend, borrow, and earn yield-all without an intermediary.

The impact was immediate: DeFi overtook ERC-20s as the dominant transaction category on-chain. Token-denominated TVL, active addresses, DEX volumes, and gas spent turned Ethereum into a real-time dashboard of decentralized finance.

It was also a turning point for Ethereum's economic flywheel. As DeFi usage surged, so did fees, developer mindshare, and validator incentives. Ethereum's network began monetizing demand for its services: providing a programmable liquidity layer for financial activities without an intermediary.

Still, DeFi's vast scale exposed strain in the ecosystem. Congestion became chronic. Gas fees spiked to levels that priced out users and applications. Ethereum was winning, but it was also breaking, it became unusable. Fees per transaction increased to $13 in 2020, $68 in 2021 and $200 in 2022.

The protocol was struggling to provide service to a small segment of the world: crypto-expert users of DeFi protocols. If Ethereum planned to be the world's programmable computer, or the rails on which the future of finance would be built, something had to change. It couldn't handle the traffic.

Vitalik proposed a novel solution in a now-legendary blog post titled "Endgame." The post outlined a vision for how Ethereum would scale. If the central blockchain couldn't handle the demand, Ethereum would allow parallel tracks, called Layer 2 networks that would blossom alongside the main chain. Like access roads running along the highway, these Layers 2s could handle the traffic Ethereum could not, and would periodically post batches of transactions to the mainnet. This would prove to be a valuable, controversial, and a consequential pivot, and vastly change the economics of Ethereum, which we will get to later.

5. The Flippening That Wasn't (2021-2025)

In 2021, Ethereum nearly flipped Bitcoin. The ETH/BTC ratio surged from ~5% to 83% in six months, marking the high point of a narrative cycle that cast Ethereum as the successor to Bitcoin-leading in users, fees, and developer activity. For a moment, it felt inevitable: Ethereum would overtake it in functionality and value.

The Flippening benchmarked Ethereum against Bitcoin. But the comparison was flawed.

Bitcoin is optimized for scarcity and monetary certainty-21 million tokens, held outside of government and institutional control. Ethereum is expressive, adaptable, and programmable. It was never built to be digital gold. Trying to “out-Bitcoin” Bitcoin was a category error.

The Flippening never materialized. The ratio retraced, bottoming at 11% by early 2025. On the surface, it looked like Ethereum had lost. In truth, Ethereum had learned.

There were significant changes to:

- Monetary policy (The Burn),

- Technological Architecture (Proof of Work to Proof of Stake),

- Scaling approach (L2s),

- Business model (transition from selling blockspace to data availability),

- Roadmap (restructuring of the Ethereum Foundation).

The next half of the report takes the reader on a rollercoaster ride over the next four years. At first it was dark. Unintended consequences from upgrades and pivots plagued the protocol in every direction it took. Other competitors began to take market share and value from Ethereum. Sentiment was destroyed, developers were disenfranchised and users lost faith.

It took years of pain, deep reflection and realisation from The Foundation to pivot not just the roadmap, but Ethereum's entire posture-from a research-driven protocol drifting on reputation, to a product-focused institutionalised platform rebuilding trust through urgency, clarity, and execution.

6. The Burn Upgrade: A New Economic Engine (2021)

One challenge Ethereum faced as an investment was “why does it have value?” The protocol addressed this head-on in an upgrade called the London Hard Fork, or EIP-1559. EIP-1559 aligned network activity and protocol value via the introduction of base fee burns. A base fee, denominated in ETH, is the minimum fee part of every transaction made by a user. These get burned and taken out of circulating supply forever. ETH supply, therefore, became dynamically tied to usage-turning transaction demand into a disinflationary, and at times, deflationary force. The protocol was no longer just rewarding validators through inflating the circulating supply; it was in effect generating buyback pressure of its own token through burn mechanics.

The results were immediate and structural:

- Annual ETH inflation rate dropped to -0.34% since the upgrade.

- Post-Merge issuance moderated to +0.12% annualised, from 4% in its Proof of Work days.

While not always net-deflationary, the burn mechanism redefined ETH's monetary policy. It introduced a feedback loop where network adoption compresses supply, anchoring ETH's value in protocol utility. This reinforced Ethereum's "Ultrasound Money" narrative and differentiated its economic model from both Bitcoin and inflationary L1 competitors.

Note: The Merge (Ethereum's transition to proof-of-stake validation) took place on September 15, 2022. As of June 30, 2025, the total supply of Ethereum was 120,866,777 ETH.

7. The Merge: Economic Security Reimagined (2022)

Ethereum's switch from Proof of Work to Proof of Stake was seven years in the making; it was even discussed and developed prior to Ethereum's launch due to environmental concerns with Proof of Work.

Changing the consensus protocol of a blockchain is hard. It is akin to swapping out the engine of an airplane in midflight. The process formally began in October 2020 with the deployment of the staking deposit contract and culminated on September 15, 2022, when the experimental staking chain (called the “Beacon Chain”) merged with Ethereum's execution layer. From that moment, Ethereum retired its miners and fully embraced staking as its transaction processing and security mechanism.

The upgrade provided multiple significant benefits to Ethereum and ETH holders:

- Reducing energy consumption by 99%.

- Escaped a doomed arms race against Bitcoin's industrial hashrate-180,000x larger-by embracing capital over computation for security.

- It now costs at least $64bn to 51% attack the network today.

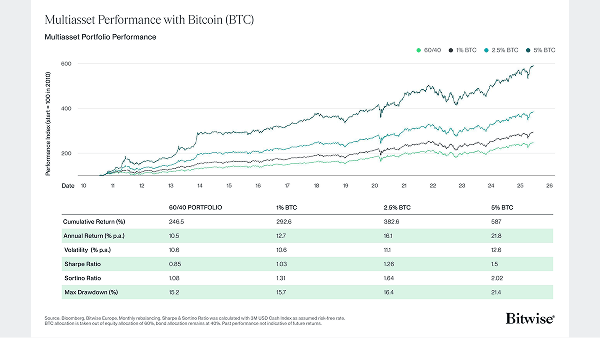

- ETH became a yield-bearing asset-one capable of anchoring institutional portfolios.

In every respect-mainly economic security and institutional financialisation-Ethereum leveled up.

8. L2 Era Begins: The Rollup Pivot (2021–2023)

Ethereum's rollup-centric roadmap delivered scale. It prevented Ethereum from losing ground entirely to newer chains like Solana and Hyperliquid. It kept users in the ecosystem-even if not directly on the mainnet.

Coinbase's L2, Base, launched in 2023, which validated Vitalik's “Endgame” post. It quickly became the most active and largest rollup by TVL, trading volume, fees, and daily users. It also brought institutional credibility to Ethereum's L2 roadmap by putting a Nasdaq-listed name on-chain.

With scale, came consequences.

The transition to Layer-2s fragmented the ecosystem across liquidity pools, tech stacks, and user experiences. Too many rollups, too little cohesion. Capital rotated out of Layer-1, R&D efforts splintered, and UX friction increased.

The Ethereum base layer also suffered as a result-activity dropped, and with it, fee burn. The “Ultrasound Money” narrative-dependent on high L1 throughput to drive ETH burn-began to lose traction.

L2 efficiency came at the cost of Ethereum's monetization model. Transaction frequency alone couldn't compensate for the diminished value of each transaction, leading to diminished value capture, rather than momentum.

9. Ethereum Wakes Up (2024 - 2025+)

By the end of 2023, Ethereum was an academically-driven behemoth–worth $276bn and down 50% from its peak–with no narrative or urgency. Other alternative Layer 1s were eating Ethereum's lunch.

Solana, for instance, which launched in 2020, was rivalling Ethereum's adoption metrics but with a more nimble developer base, start-up mindset focused on the user, and excited long-term institutional capital supporting architectural developments to applications building on top.

Ethereum, on the other hand, was tying themselves up in knots. It failed to compete with Solana and alt-L1s on cost, speed and UX-domains where those chains were purpose-built. Simultaneously touting its deflationary mechanics and “Ultrasound Money” thesis to rival Bitcoin on its monetary purity. As mentioned earlier, this also ended up failing due to L2 fee extraction, capital rotation, and R&D and mindshare splintering.

In chasing both rabbits, Ethereum caught none.

To make matters worse, internal voices began to criticize its long-term roadmap-like Justin Drake's Beam Chain proposal, which pushed full implementation into the 2030s. For many, the protocol felt more like a vision than a mission-a map that took the focus off building in the present, and in turn exposing Ethereum to the real possibility of falling behind the wayside forever.

After the backlash to this proposal, Ethereum's cultural posture began to change. The Ethereum Foundation announced leadership restructuring with a focus on three main objectives: scaling Ethereum's Layer 1, enhancing data availability through "blobs" to scale Ethereum's Layer 2s, and significantly improving user experience. Layoffs also occurred to streamline the Foundation and improve alignment and communication. The creation of a new business development and marketing function aims to enhance institutional adoption.

The Pectra upgrade, deployed in May 2025, doubled Blob throughput. The next upgrade, Fusaka, is expected in November 2025 and has been pulled forward marginally. As of writing, PeerDAS takes center stage-anchor scaling through Data Availability Sampling–to further extend throughput on top of the progress made in Pectra. Less critical upgrades like EOF remain but may be trimmed if needed to preserve timeline integrity. Scope reductions are strategic, not signals of slippage.

Ethereum has woken up, regained focus and found narrative clarity.

Ethereum has built the infrastructure to support a modular, institution-ready future. But with blob throughput scaling faster than usage, L2 settlement costs are falling-compressing one of Ethereum's few native revenue streams. It's a sign the system is working, but also a signal of what comes next. To fulfill its ambition as civilization-grade infrastructure, Ethereum must now solve for pricing power-turning blob fees into a dependable, elastic source of protocol revenue.

10. Institutional Inroads: ETF Era, Stablecoin Boom, Treasury Companies (2024 - 2025+)

The protocol's composability, decentralization, liquidity, brand-name, uptime and reliability made it a natural choice for institutions building on and using decentralised finance rails.

That shift accelerated dramatically with the passage of the Genius Act, the United States' first major stablecoin regulatory framework. Suddenly, Ethereum was the backbone of compliant, internet-native dollars.

The majority of on-chain stablecoin and tokenized asset activity already lived on Ethereum. It had quietly captured more than 50% of the stablecoin market cap and over 55% of all tokenized value. The infrastructure was in place long before the legislation. The Act simply turned the spotlight on.

Institutions noticed. In the two weeks leading up to the bill's passage, ETHBTC rotation spiked-proof that investors were potentially front-running the regulatory shift.

Corporate adoption trends have accelerated, with Ether treasury companies gaining prominence and contributing to outperformance. The Ether Machine's combination with Dynamix Corp, a NASDAQ SPAC, launched with over 400,000 Ether valued at $1.45 billion at current prices-representing nearly half of the $3 billion held by publicly traded companies (886,060 Ether total).

Net ETH ETF flows have reached all-time highs, totalling $2.1 billion in the second week of July 2025. This is institutional recognition of Ethereum's role as "Digital Oil" powering tokenization and stablecoin infrastructure.

With regulatory clarity emerging, institutional onboarding and liquidity dominance, Ethereum's next wave of capital won't be chasing returns. It will be underwriting the system itself.

Bottom Line

- Ethereum’s greatest strength is its ability to adapt without losing coherence, evolving through cultural forks, architectural pivots, and economic redesigns that most platforms wouldn’t survive.

- Ethereum’s architecture and economic model has pivoted a few major times to combine network adoption and value capture, and improve validator and user experience.

- With regulatory clarity, stablecoin rails, DeFi dominance, RWA applications and ETF flows converging, Ethereum isn’t chasing the next narrative—it’s aiming to become the institutional foundation that underwrites it.

Informazioni importanti

Le informazioni contenute nel presente materiale hanno finalità esclusivamente illustrative o informative e non costituiscono consulenza in materia di investimenti, raccomandazione personalizzata, né un’offerta o sollecitazione al pubblico risparmio.

Il presente documento (che può assumere la forma di presentazione, comunicato stampa, post sui social media, articolo di blog, comunicazione audiovisiva o altro strumento analogo – di seguito, per semplicità, “Documento”) è emesso da Bitwise Europe GmbH (“BEU” o “l’Emittente”) ed è redatto in conformità alla normativa applicabile, incluse le disposizioni in materia di comunicazioni promozionali relative a strumenti finanziari.

Bitwise Europe GmbH, costituita secondo il diritto tedesco, è l’emittente degli Exchange Traded Products (“ETP”) descritti nel presente Documento ai sensi di un prospetto di base e delle relative condizioni definitive, eventualmente integrati nel tempo e approvati dalla Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin). L’approvazione del prospetto da parte di BaFin non costituisce un giudizio di merito sull’investimento né un’approvazione del presente contenuto da parte di CONSOB.

Prima di effettuare un investimento in prodotti emessi da BEU, è opportuno verificare con i propri consulenti professionali e con il proprio intermediario che tali prodotti siano disponibili nella propria giurisdizione e coerenti con il proprio profilo di rischio. Ogni decisione di investimento dovrebbe essere assunta tenendo conto della propria situazione personale, dopo aver ottenuto consulenza indipendente di natura finanziaria, fiscale e legale.

Capitale a rischio. Le cripto-attività sono strumenti ad elevato rischio e caratterizzati da elevata volatilità. Il valore degli investimenti in cripto-attività e in ETP con esposizione a cripto-attività può diminuire così come aumentare e gli investitori possono perdere parte o la totalità del capitale investito. Nessun sistema di garanzia o indennizzo protegge dalle perdite derivanti dall’andamento di mercato. Le performance passate non sono indicative di risultati futuri. Le dichiarazioni previsionali non costituiscono garanzia di risultati.

Prima di investire, si raccomanda di leggere attentamente il prospetto di base e le relative condizioni definitive, in particolare la sezione “Fattori di rischio”, disponibili sul sito https://bitwiseinvestments.eu/it/

L’accesso a determinati documenti può richiedere una dichiarazione in merito alla propria giurisdizione e alla propria categoria di investitore e può essere soggetto a ulteriori avvertenze e informazioni importanti.

Ulteriori informazioni sui rischi sono disponibili al seguente indirizzo: https://bitwiseinvestments.eu/it/risk-warning/